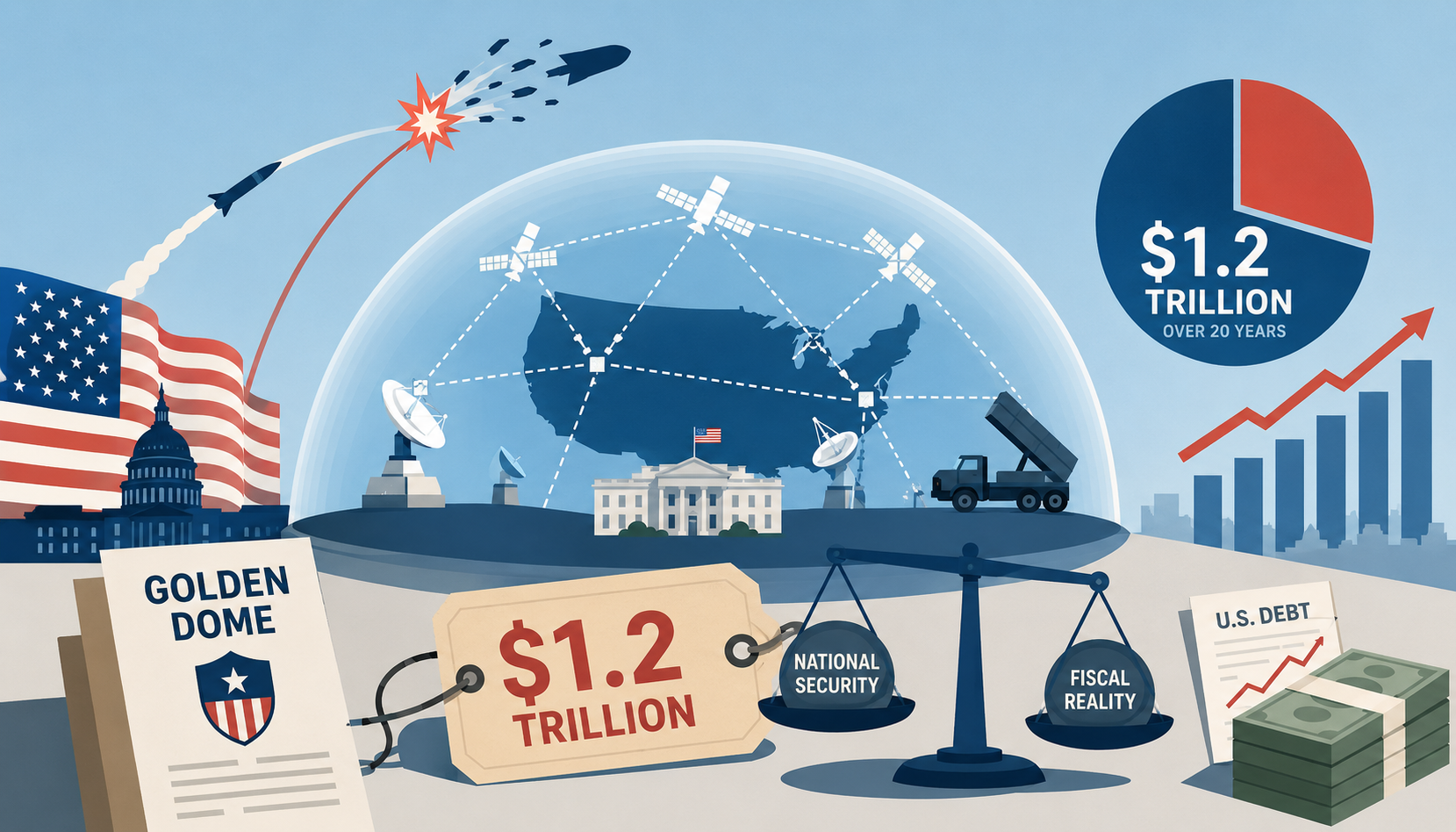

A missile shield sounds like a military project. A $1.2 trillion missile shield is also an economic event.

That, in essence, is what changed this week. On Tuesday, the Congressional Budget Office released a 12-page analysis estimating that President Trump’s “Golden Dome for America” missile defense program would cost roughly $1.2 trillion to develop, deploy, and operate over the next two decades. The figure is more than six times higher than the $185 billion that Gen. Michael Guetlein, the Pentagon officer running the program, cited earlier this year, and almost seven times the $175 billion that Trump originally floated when he signed the founding executive order in January 2025.

Numbers that big tend to escape the defense pages. They land in the bond market, the budget debate, and the long-running argument over how much fiscal space the United States still has left.

Three numbers, one widening gap

It helps to line the estimates up:

- $175 billion — Trump’s original public figure, cited when the project was launched.

- $185 billion — the Pentagon’s working estimate from March, anchored in what Guetlein has called an “objective architecture” through the mid-2030s.

- $1.2 trillion — the CBO’s new 20-year estimate for an architecture broadly consistent with the executive order.

The CBO is careful about its own number. The agency notes that the Defense Department has released few public details about the actual system it intends to build, and that its analysis therefore rests on a “notional” architecture inferred from the executive order. The gap between $185 billion and $1.2 trillion, the report suggests, could reflect a more limited objective design, the Pentagon’s expectation of pulling significant funding from other accounts, a shorter time horizon — or some combination of the three.

In other words, the most important fact in the report may not be the headline. It is the uncertainty. A program with this much architectural ambiguity, this far into the budgeting cycle, is unusual even by the standards of large defense procurements. Congress is now being asked to fund something whose blueprint remains a moving target.

Why space is doing most of the damage

Roughly 70 percent of acquisition costs in the CBO’s scenario sit in a single component: a constellation of space-based interceptors — satellites armed to strike enemy missiles in the boost phase, just after launch.

The math is brutal. To engage a barrage of about 10 nearly simultaneously launched intercontinental ballistic missiles in their boost phase, the CBO estimates the Pentagon would need around 7,800 satellites in low-Earth orbit. That single layer alone would run to about $720 billion over 20 years, plus around $1 billion a year just to operate.

Even Guetlein has signaled that this may be more than the program can absorb. In April, he told the House Armed Services Strategic Forces subcommittee that if boost-phase intercept from space is not affordable and scalable, “we will not produce it.” That is a significant admission from the program’s own director, and it hints that the final Golden Dome may look different from the system the CBO costed.

The deeper economic point is structural. A space-heavy architecture turns missile defense from a one-off procurement into something closer to a permanent industrial program. Satellites have to be launched, replenished, maintained, hardened against jamming and anti-satellite weapons, and tied into a continuously updated command-and-control stack. That is closer in spirit to running an airline than to buying a fleet of tanks. Cost curves bend accordingly.

A new pressure point on the fiscal outlook

Spread evenly, $1.2 trillion over 20 years works out to about $60 billion a year. Actual spending would lump heavily into the first decade, when most acquisition occurs, but the average is still useful as a back-of-the-envelope.

Sixty billion a year does not, on its own, move the U.S. fiscal trajectory. The Trump administration has already requested $1.5 trillion in total defense spending for fiscal 2027, of which roughly $750 billion is earmarked for missile defense, drones, AI, and the broader defense industrial base. Against that backdrop, Golden Dome is one large line item among many.

But the program is being layered on top of a fiscal picture that is already crowded. Interest costs on federal debt are at multi-decade highs. Entitlement spending continues to grow on autopilot. The defense budget itself has reached levels that, in nominal terms, would have been unthinkable a few years ago. Each new long-term commitment narrows the space for the next.

That is why a project like Golden Dome matters to bond investors even if no single year’s outlay is dramatic. It contributes to the same fiscal narrative that has been pushing term premia higher and forcing the Treasury to issue more long-dated paper into a less captive buyer base. Golden Dome alone will not move 10-year yields. The pattern of which it is a part might.

Senator Jeff Merkley, the Oregon Democrat who requested the CBO report as ranking member of the Senate Budget Committee, framed the program in starker terms, calling it “a massive giveaway to defense contractors paid for entirely by working Americans.” That is a partisan reading. But it is also a preview of the political fight that will shape how Congress chooses to finance the project — through dedicated appropriations, reconciliation, or simply more borrowing.

Defense stocks: a clearer signal than the macro

For equity investors, the picture is less ambiguous than it is for bond investors. Major defense primes — Lockheed Martin, Northrop Grumman, RTX, and Boeing — are expected to compete for components across the system. The U.S. Space Force has already awarded contracts worth up to $3.2 billion to 12 companies to develop space-based interceptor prototypes, with the long-term production pipeline potentially worth $1.8 billion to $3.4 billion a year.

Lockheed has already won space-based interceptor contracts and sits at the center of the missile-defense ecosystem. Northrop’s expertise in integrated battle command makes it a natural prime for the command-and-control layer. RTX, through its Raytheon business, brings radars and interceptors. Newer players — Anduril, True Anomaly, and an eventually public SpaceX — round out a contractor base that looks notably broader than the Cold War missile-defense roster.

The implication is straightforward but worth stating carefully. Golden Dome may be bullish for selected defense and space names, particularly those positioned on the satellite and AI-enabled tracking side of the program. It is less clearly bullish for the broader macro backdrop, where it adds to Treasury supply pressure and complicates any narrative of fiscal consolidation.

Defense ETFs such as ITA and PPA have already had a strong year. The question for investors is no longer whether the spending cycle is real, but how to separate companies with durable Golden Dome content from those that will benefit only at the margin.

Will it work, and against whom?

Cost is only half of the controversy. The CBO is also blunt about effectiveness. The notional architecture it modeled could engage a limited attack from a regional adversary such as North Korea, or a smaller barrage from China or Russia. But the agency warns the system “could be overwhelmed by a full-scale attack mounted by a peer or near-peer adversary,” and that “‘fully engage’ is not the same as ‘fully defeat’ because no defense works perfectly every time.”

That creates an awkward editorial question for the program’s backers. If Golden Dome is mainly a shield against limited regional threats, is $1.2 trillion politically defensible? If it is meant to neutralize peer nuclear forces, the CBO suggests the technology is not there. And if adversaries respond by expanding their missile arsenals or investing more heavily in anti-satellite weapons, the project could intensify the very threat it is meant to contain.

These are not new concerns in missile-defense debates. They are, however, sharper this time because the project’s space-based design pushes the arms-race logic into orbit, where the rules and the costs are still being written.

A shield, a subsidy, or a fiscal gamble?

Golden Dome can be read in three ways at once. It is a homeland security shield, intended to protect the continental United States, Alaska, and Hawaii against ballistic, hypersonic, and cruise missiles. It is an industrial-policy subsidy, channeling tens of billions of dollars a year into a defense-and-space sector that increasingly resembles the country’s most strategic industrial cluster. And it is a long-term fiscal gamble whose returns — strategic, technological, and budgetary — will not be fully known for decades.

The CBO has done Congress a useful service by forcing the second and third readings into the open. The most important number in the report may not be $1.2 trillion. It may be the widening gap between what political leaders have promised Golden Dome will cost and what it is likely to cost once the architecture is real. Closing that gap, in Washington or in the Treasury market, is the work that comes next.