ADNOC’s plan for a new multi-fuel pipeline is more than an infrastructure headline. Coming roughly three months into an active Strait of Hormuz crisis, it is a signal that Gulf exporters have stopped treating the strait as a permanently reliable artery — and are now willing to commit capital to that view.

Why the ADNOC Pipeline Plan Matters

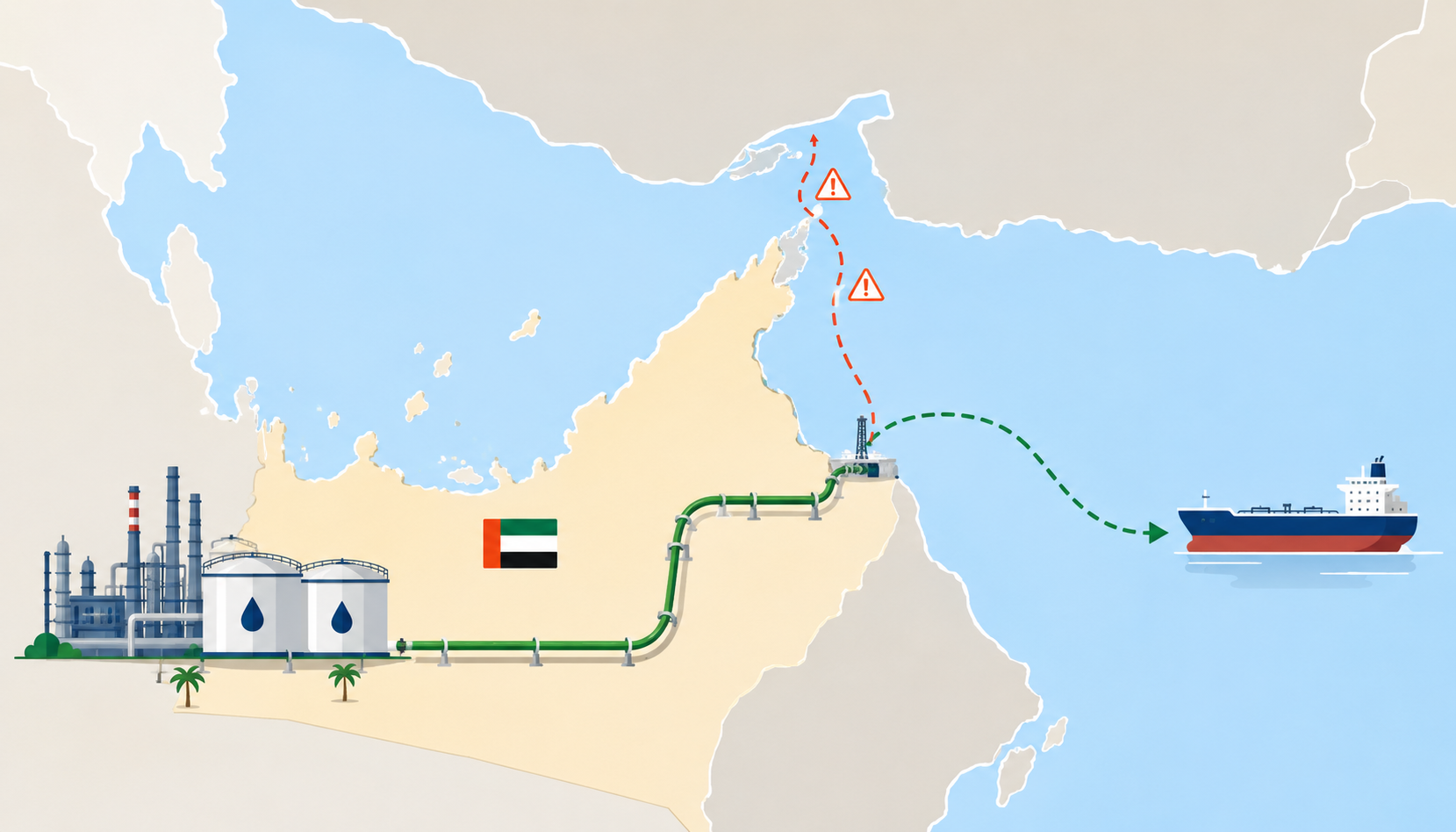

According to the Financial Times, Philippe Khoury, ADNOC’s executive vice president for sales and trading, told the Middle East Petroleum and Gas Conference in London that the company is planning a pipeline able to move refined products — gasoline, diesel and jet fuel — to an export point that sits outside the Strait of Hormuz. He did not give a timeline or a precise location, but said it would complement ADNOC’s existing Habshan–Fujairah system. Reporting on the comments described a line designed to switch between products, conceptually closer to the U.S. Colonial Pipeline than to a single-grade crude route. ADNOC already markets a full slate of refined products — diesel, gasoline, naphtha, jet fuel, fuel oil — so the proposal is about moving those barrels around a chokepoint, not entering a new business.

The product focus is the part worth slowing down on. Crude has to be refined before it reaches anyone; a crude interruption works through the system over months. Refined products are finished fuels that flow straight into consumption. A disruption to gasoline, diesel and jet fuel shows up at the pump, the airport and the freight depot in weeks, and it feeds directly into headline inflation and transport costs. Building redundancy for products, not just crude, is a quiet admission that the fast-moving end of the barrel is where a chokepoint shock actually bites.

It is also a distinct project from the crude line ADNOC has been racing to finish. In a 20 May interview with the Atlantic Council, CEO Sultan Al Jaber said a second crude pipeline to Fujairah was nearly half built and being accelerated, with the Abu Dhabi Media Office putting commissioning in 2027. That line would roughly double the 1.8 million barrels per day of crude the UAE can already route past the strait. The new multi-fuel proposal layers product resilience on top of crude resilience. Two pipelines, two different parts of the supply chain, one strategic idea.

Hormuz as a Global Energy Chokepoint

To see why this matters, start with the baseline. EIA’s World Oil Transit Chokepoints data show that oil flows through the Strait of Hormuz averaged about 20.9 million barrels per day in the first half of 2025 — roughly a fifth of global petroleum liquids consumption. Of that, around 14.7 million b/d was crude and condensate and about 6.1 million b/d was refined products, alongside the bulk of the region’s LNG. The IEA puts the 2025 figure near 20 million b/d, with crude alone accounting for close to 34% of global crude oil trade. China and India together took roughly 44% of the crude leaving the strait. Critically, EIA notes that only Saudi Arabia and the UAE operate crude pipelines capable of bypassing Hormuz at all.

Those are pre-war numbers, and they no longer describe reality. Since strikes on Iran began in late February 2026 and Tehran effectively closed the waterway, transit has collapsed. EIA’s new Global Energy Security Data report shows first-quarter 2026 flows down nearly 30% year on year, to about 14.6 million b/d. The IEA’s May 2026 Oil Market Report is starker: with tanker traffic still restricted, more than 14 million b/d of Gulf oil sat shut in and cumulative Gulf supply losses had passed one billion barrels, which the agency called an unprecedented supply shock. Dated Brent averaged around $120 a barrel in April and touched an all-time high near $145 earlier that month. This is the backdrop against which ADNOC is choosing what to build next.

The UAE’s Strategic Logic

Fujairah is the reason the UAE has options most of its neighbours lack. The port sits on the Gulf of Oman, just beyond the strait, which means barrels reaching it never have to thread the chokepoint. Through the crisis, the UAE has been a relative winner: the IEA reports that Abu Dhabi redirected volumes to Fujairah and that loadings there rose, while Saudi Arabia leaned on its Red Sea outlets at Yanbu and Muajjiz. Al Jaber’s framing at the Atlantic Council was blunt — too much of the world’s energy, he said, still moves through too few chokepoints.

The strategic logic is straightforward. Redundancy reduces the leverage that any hostile actor — or any single accident — can exert over UAE export revenue. The crude pipeline addresses the upstream side; the refined-product line, if built, would close a gap on the downstream side. The UAE can attempt this because it has the east-coast geography, a $150 billion five-year capital programme behind it, and the strongest credit standing in the sector. The harder question is whether others can follow: Kuwait, Qatar and Bahrain remain almost entirely dependent on the strait, with little comparable bypass capacity.

Market Implications

- Oil and product prices. A second bypass route lowers the long-run tail risk attached to UAE-linked supply. It does little for the near term — the product line has no announced timeline, and a pipeline on paper moves no barrels during the current crisis.

- Shipping and insurance. Over time, credible onshore alternatives could ease war-risk premiums on some Gulf-of-Oman routes. That benefit is gradual and contingent on the infrastructure actually being protected and operational.

- Credit and sovereign risk. Demonstrated ability to keep exporting through a chokepoint shock supports the UAE’s fiscal and current-account resilience, and by extension the credit profile of its sovereign and quasi-sovereign issuers.

- Regional competition. Saudi Arabia already runs its East–West crude line; the ADNOC moves raise the pressure on Gulf peers to reassess bypass capacity — though for products specifically, options are thin across the region.

Limits and Risks

A pipeline does not remove regional risk. It relocates it. Moving exposure from a maritime chokepoint to fixed onshore infrastructure trades tanker-route vulnerability for the security of pumping stations, terminals and the route itself. The IEA has noted that existing bypass options through Fujairah and the Red Sea remain vulnerable to attack, and a refined-product corridor would carry the same physical, drone, sabotage and cyber exposure.

Capacity is the other constraint. Bypass infrastructure has never been sized to replace normal Hormuz throughput; even the doubled crude capacity falls well short of pre-war flows, and a product line would be smaller still. Construction timelines, financing and operational complexity all argue for caution. With no schedule attached to the multi-fuel proposal, it is best read as direction of travel rather than near-term supply relief.

Analyst’s View

From a country-risk seat, the signal matters more than the steel. The UAE’s capacity to sustain exports during a chokepoint crisis is a direct input into fiscal resilience, current-account strength and investor confidence — and therefore into how one prices UAE sovereign and quasi-sovereign credit. A credible refined-product bypass marginally lowers the probability of a severe, prolonged revenue interruption, which feeds through to lower expected loss on UAE-linked exposures in an IFRS 9-style framework. The effect is real but bounded: an announcement is not operational capacity, and operational capacity is not crisis-scale throughput. Those three things should be tracked separately.

The sharper point for risk practitioners is that the risk does not disappear — it migrates. As the UAE shifts barrels from the strait to fixed corridors, the binding constraint becomes the physical and cyber security of Fujairah and the inland routes feeding it. That argues for re-weighting exposure analysis away from pure maritime-chokepoint scenarios and toward onshore-infrastructure and drone-threat scenarios. And none of this de-risks the neighbours: Qatar, Kuwait and Bahrain still lack equivalent escape routes, so the credit gap between UAE-linked and other Gulf exposures is likely to widen, not converge, the longer chokepoint risk stays elevated.

The deeper story, then, is not “UAE builds another pipeline.” It is the repricing of energy-security infrastructure in a more fragmented world. Redundancy that looked like an optional cost in 2024 now reads as a balance-sheet asset — and the producers without it are discovering how expensive its absence can be.