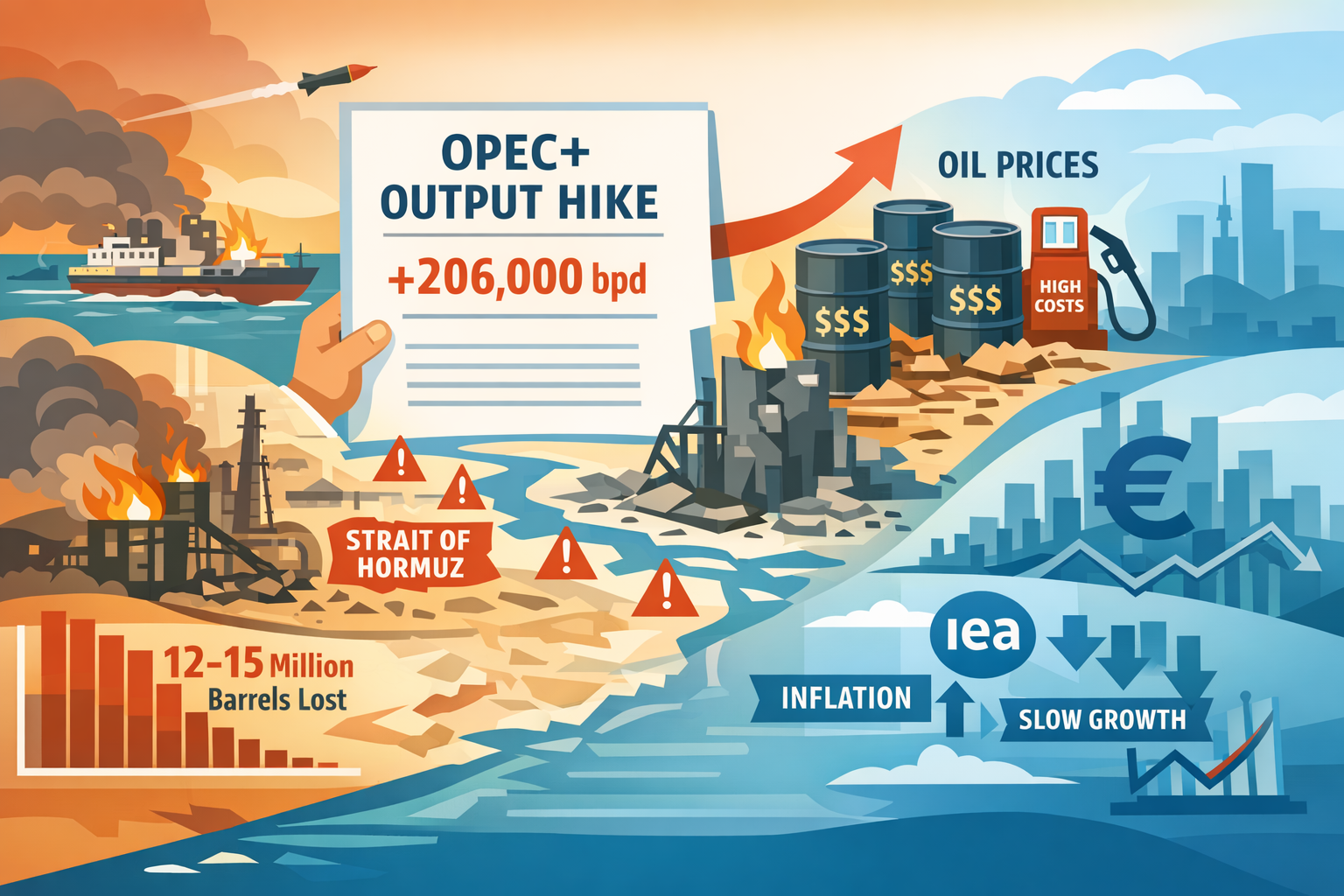

Eight OPEC+ countries agreed on April 5 to lift production quotas by 206,000 barrels per day for May 2026. On any normal day, that would be the kind of move markets reward with a sigh of relief. This is not a normal day.

The Strait of Hormuz—through which roughly a fifth of the world’s oil supply typically flows—remains heavily disrupted by the ongoing US-Israeli military campaign against Iran. Key Gulf export terminals have sustained physical damage. Shipping insurers have pulled back. And the alliance’s own communiqué carried an unusual line for a supply decision: it stressed the “critical importance of safeguarding international maritime routes” for uninterrupted energy flows.

In other words, OPEC+ raised the ceiling. But the floor—the infrastructure, the tanker routes, the loading docks—is broken.

More barrels on paper

The 206,000 bpd increase is part of OPEC+’s broader phase-out of voluntary production cuts, and the group was careful to signal flexibility. It can accelerate, pause, or reverse the unwinding depending on conditions. That language is standard, but this time it reads less like cautious policy management and more like an acknowledgment that the decision may not translate into physical barrels any time soon.

Reuters described the increase as likely to exist “on paper” under current wartime conditions. Jorge Leon of Rystad Energy was blunter: “In reality it adds very few barrels to the market.”

That framing matters. Quota changes only affect supply when producers can actually extract, process, and ship crude. Right now, several of the Gulf’s largest exporters face constraints on at least one of those steps.

The bottleneck is not wells—it’s water

The real chokepoint is not production capacity. It is transit. The Strait of Hormuz is narrow, shallow, and currently a conflict zone. Even where select vessels have been able to pass—Japan’s Mitsui O.S.K. Lines managed to move tankers through under diplomatic cover—the broader shipping picture remains severely impaired. War-risk insurance premiums have spiked, and many operators are simply avoiding the route altogether.

OPEC itself seemed to recognize this when it highlighted maritime security in its statement. That is not normal language for a production decision. It signals that the alliance understands the constraint is logistical, not geological.

Damage that outlasts the fighting

Even if a ceasefire materialized tomorrow, the supply picture would not normalize quickly. OPEC warned that restoring damaged energy infrastructure is costly and time-consuming. Gulf officials quoted by Reuters said a return to normal operations could take months.

This is an underappreciated point. Markets tend to price in conflict as a binary—on or off. But energy infrastructure does not work that way. Export terminals, pipeline junctions, desalination-dependent processing plants, and port facilities all require sustained, specialized repair. The physical capital stock of Gulf oil production is not something that snaps back with a diplomatic handshake.

What prices are actually saying

If the quota increase were meaningful, you would expect to see some softening in crude benchmarks. Instead, Brent traded at $108.39 and WTI at $110.21 on April 6—still elevated after the prior session’s surge, which marked the biggest absolute daily price jump since 2020.

More telling than headline prices is the premium structure. Saudi Arabia raised its May Official Selling Price for Arab Light to Asia by a record $19.50 per barrel above the Oman/Dubai benchmark. That is not a producer expecting slack in the market. It is a producer that knows its barrels are scarce and is pricing accordingly.

Taken together, the price and premium signals suggest traders see the same thing the data shows: physical supply remains far tighter than any quota adjustment can fix.

The scale mismatch

Here is where the arithmetic becomes stark. Reuters estimated that the wartime disruption has removed somewhere between 12 and 15 million barrels per day from global supply—up to 15 percent of the world’s pre-conflict output. Against that, a 206,000 bpd quota increase covers roughly 1.5 percent of the shortfall.

The IEA’s chief, Fatih Birol, put a finer point on the trajectory: “The loss of oil in April will be twice the oil loss in March.” That is not a market that is stabilizing. It is a market where the gap between supply and demand is still widening.

From oil shock to inflation shock

This is where the story leaves the commodity desk and enters the macro economy. The IEA warned that the disruption would feed into inflation and weaken growth across multiple regions, with the impact spreading from Asia—where Gulf crude dependence is highest—into Europe.

The transmission mechanism is straightforward. Tighter physical oil supply drives up fuel costs. Fuel costs feed into transport, manufacturing, food logistics, and electricity generation. Central banks that had been cautiously easing now face renewed pressure to hold rates or even reverse course. For consumers, the result is higher prices at a moment when pandemic-era savings buffers are largely exhausted.

None of this is hypothetical. It is the sequence that played out in 2022 after Russia’s invasion of Ukraine, and the current disruption is, by several measures, larger in scale.

What OPEC+ is really doing

Strip away the headline and the 206,000 bpd figure, and OPEC+’s decision reads more like a political signal than an operational one. The alliance is telling the market: we are not hoarding supply. We are willing to release barrels. The constraint is not us.

That message is directed partly at consuming nations—particularly in Asia and Europe—and partly at Washington, which has historically pressured the group to pump more during price spikes. By raising quotas while physical delivery remains constrained, OPEC+ shifts the narrative. The bottleneck is the war, not the cartel.

Whether that framing holds depends on how long the disruption lasts and how quickly alternative shipping routes or strategic reserves can compensate. So far, the gap between what OPEC+ has authorized and what the market can actually absorb remains vast.

The quota went up. The oil, for now, mostly stays where it is.