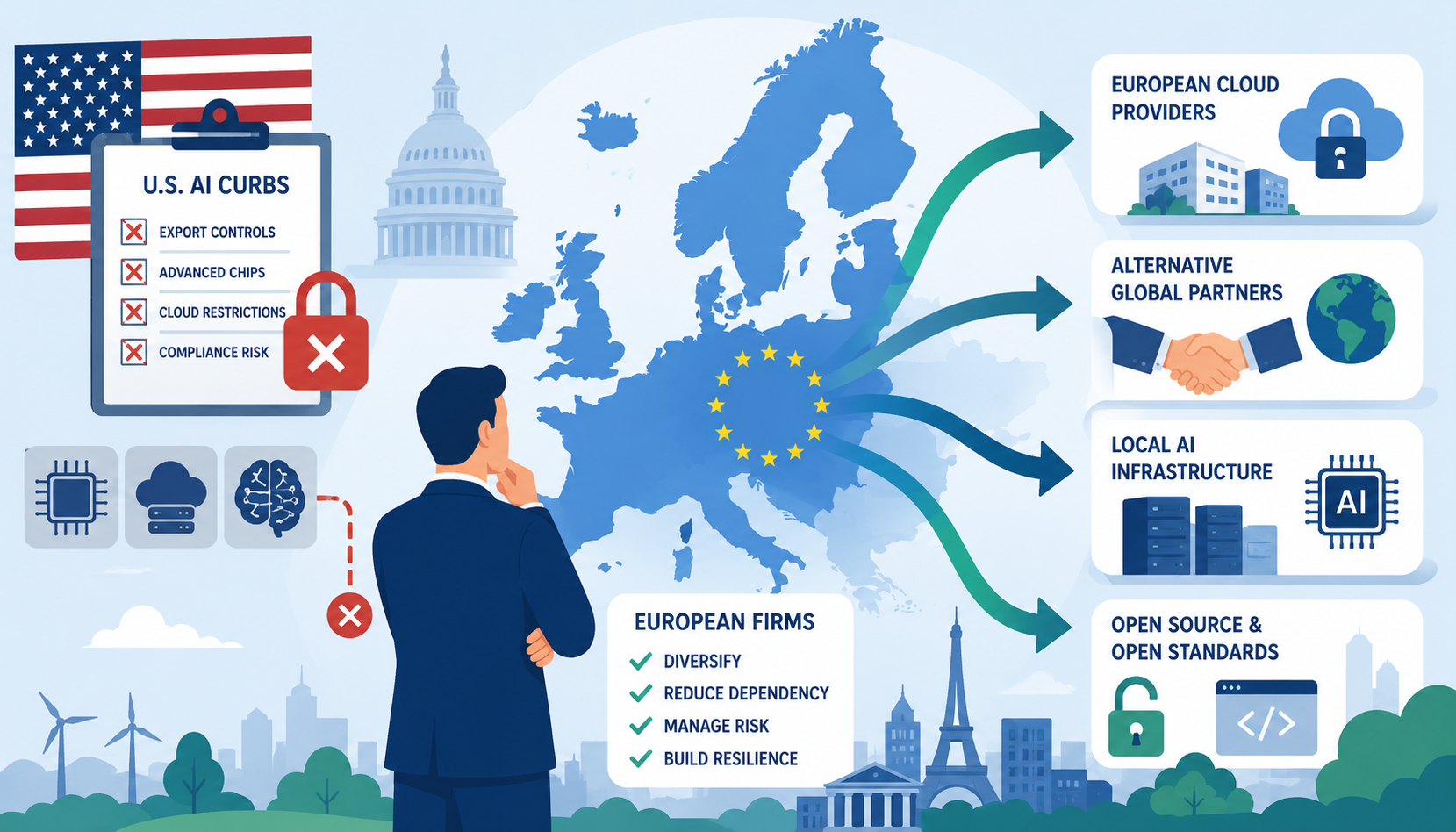

Europe’s AI ambitions are increasingly being shaped not only by innovation, but by geopolitical risk. As U.S. restrictions tighten around advanced AI technologies, European firms are reassessing where their chips, cloud capacity, models, and critical software come from — and the answer, more and more, is “not from any single place.”

The trigger for the latest round of soul-searching was concrete. Reuters reported from Paris on June 22 that limits on access to some U.S. artificial intelligence services are pushing major European companies to speed up spreading risk across multiple providers and to push harder for domestic alternatives. What made the warning land was the specific event behind it: the U.S. Commerce Department used national security export controls to bar Anthropic from distributing its newest models, Fable 5 and Mythos 5, to any foreign national — a directive Anthropic detailed in its own statement. Washington has used export controls before to restrict the semiconductor chips that power AI models, but never on the models themselves. Investing.com Canada + 2

That distinction matters. A remotely delivered, proprietary model can be switched off by its provider at the stroke of a regulator’s pen, and it cannot be run independently on a company’s own servers. For a European treasurer or CIO, that is no longer an abstract risk — it is an operational dependency with a single point of failure.

Why U.S. curbs matter

The Anthropic case sits on top of a fast-moving export-control regime. After the Trump administration rescinded the Biden-era “AI Diffusion Rule” in May 2025, Washington rebuilt the framework piece by piece. A BIS final rule effective January 15, 2026 shifted licensing for Nvidia H200- and AMD MI325X-equivalent chips destined for China and Macau from a presumption of denial to case-by-case review (Federal Register doc 2026-00789). But the relaxation came wrapped in conditions: a 25% tariff, a volume cap of 50% relative to U.S. domestic shipments, mandatory third-party testing in the United States, and know-your-customer compliance, with reexport licenses still under a presumption of denial. Federal RegisterInformed Clearly

For European firms, the headline is less about China and more about the machinery itself. The rules show that access — to chips, to compute, and now to frontier models — can be re-priced or revoked on short notice. Enforcement capacity is rising too: Congress approved a 23% increase in the BIS budget for fiscal 2026, with funds earmarked for semiconductor-related enforcement. Compliance is becoming a permanent line item, not a one-off legal review. Morrison Foerster

Europe’s diversification response

Brussels had already been moving. On June 3, 2026, the European Commission unveiled its European Technological Sovereignty Package, built around two legislative proposals — a Chips Act 2.0 and a Cloud and AI Development Act (CADA) — plus an Open Source Strategy. The scale of the dependency it is trying to correct is striking. By the Commission’s own accounting, U.S. cloud companies control more than 70% of the EU cloud market, the EU produces less than 10% of global semiconductors, and the bloc spends roughly €264 billion a year, mostly on U.S. proprietary IT products and services. Tech Policy Press

The policy answer is part money, part architecture. The investment gaps cited run to €120 billion for semiconductors, €200 billion for data centers by 2036, and €100 billion for cloud and AI, with the InvestAI initiative aiming to mobilize €200 billion. CADA aims to roughly triple EU data-center capacity within five to seven years and introduces a Cloud Sovereignty Framework that grades providers on ownership, control, data handling, and cybersecurity. A central concern is extraterritoriality — that providers could be compelled by third-country law, widely understood to mean the U.S. Cloud Act, to hand over data stored in Europe. Commission officials have framed the goal bluntly: no outside provider should hold a “kill switch” over Europe’s critical systems. Tech Policy Press + 2

Corporate behavior is running ahead of the legislation. Executives from Siemens, Renault Group, Orange and ChapsVision told Reuters at the VivaTech conference that they already blend U.S., Chinese and European models — Siemens, for instance, uses China’s DeepSeek and Alibaba’s Qwen alongside Nvidia’s Nemotron. Notably, the corporate read of “sovereignty” is narrower than the political one. Siemens digital-industries chief Cedrik Neike argued that sovereignty is often confused with autarky — and that self-sufficiency is the wrong goal. For most firms, resilience means optionality across vendors, not a walled European garden. Yahoo FinanceYahoo Finance

Market implications

The likely winners are the providers of optionality. European cloud operators, sovereign-cloud offerings, cybersecurity vendors, compliance technology, and open-source AI stacks all stand to benefit from procurement rules that reward local control and from boards newly willing to pay for a second supplier.

The costs are equally real, and worth stating plainly rather than glossing. Running multiple model providers and duplicating infrastructure raises unit costs and engineering overhead. Fragmented standards can slow AI adoption precisely when productivity gains depend on speed. And much of the European package remains a proposal: the original Chips Act took about two years from proposal to adoption, and CADA — touching the politically sensitive question of sovereignty toward key trading partners — may face comparable friction. Diversification buys insurance; like all insurance, it is a drag on margins until the day it pays out. Digital Watch Observatory

The geopolitical frame

None of this is happening in a vacuum. The export-control architecture Europe is reacting to was designed primarily for the U.S.–China technology contest, and Europe is caught in an awkward middle: a security ally of Washington that nonetheless wants strategic autonomy from it. The Anthropic episode crystallized that discomfort — a measure aimed at “foreign nationals” swept in close allies, and several European policymakers read it as confirmation that AI access is now a sovereignty question, not just a procurement one.

Analyst’s View

From a country-risk and credit perspective, three implications stand out — and none of them are generic.

Operational concentration is now a board-level credit factor. A corporate borrower whose core workflows depend on a single foreign model or cloud — one that a regulator can disable on a Friday evening — carries continuity risk that belongs in the qualitative overlay, not the footnotes. Lenders and rating analysts should be asking issuers a concrete question: if your primary AI or cloud provider were cut off tomorrow, what is the substitution time, and what does it cost? Firms without a credible answer warrant a wider risk premium.

Sovereign and quasi-sovereign exposure shifts with the subsidy map. Europe’s €100–200 billion in mobilized cloud, AI, and chip spending will reshape state contingent liabilities and the credit profiles of the national champions and data-center operators that absorb it. For a development-finance or project-finance lender, the relevant risk is execution: these are long-dated, capital-intensive builds whose returns depend on demand materializing and on legislation surviving 27-member-state negotiation. Policy-reversal risk is the binding constraint, not technology risk.

The macro backdrop caps the upside. This is where the practitioner should resist optimism. IMF staff analysis finds that adding technological decoupling to trade fragmentation could push output losses to 8–12% of GDP in some countries (IMF, Geoeconomic Fragmentation and the Future of Multilateralism). Europe may gain strategic optionality and a stronger domestic supply base, but duplicate infrastructure and compliance complexity are a structural tax on the continent’s productivity — and, by extension, on the debt-servicing capacity of the firms and sovereigns inside it. International Monetary Fund

The practical takeaway for risk managers is unglamorous but durable: treat AI-supply resilience the way you already treat funding and FX. Map the single points of failure, price the substitution cost, and assume the rules will change again before your exposure rolls off. Europe’s firms have started doing exactly that — not because diversification is cheap, but because the alternative just demonstrated, in real time, that it can be switched off.

SEO Title: US AI Curbs Push European Firms to Diversify Tech Risk

Meta Description: U.S. AI restrictions are pushing European firms to diversify technology risk, reshaping supply chains, cloud strategy, and market exposure.

Meta Keywords: US AI curbs, Europe AI, technology risk, AI supply chain, export controls, cloud strategy, digital sovereignty