The International Monetary Fund’s latest read on the world economy is a study in tension. War in the Middle East is dragging on growth. A wave of investment in artificial intelligence is pulling in the other direction. In its July 2026 World Economic Outlook Update, released on 8 July, the Fund keeps global growth at 3.0 percent for 2026 and 3.4 percent for 2027 — down from the 3.5 percent average of 2024–25, but, notably, little changed from its April forecast on a cumulative basis. The reason it held steady is the headline of the report: the drag from war is being partly offset by the momentum of the global technology cycle.

That is the optimistic half of the story. The IMF is equally clear that the same forces cushioning the blow today could be seeding tomorrow’s instability.

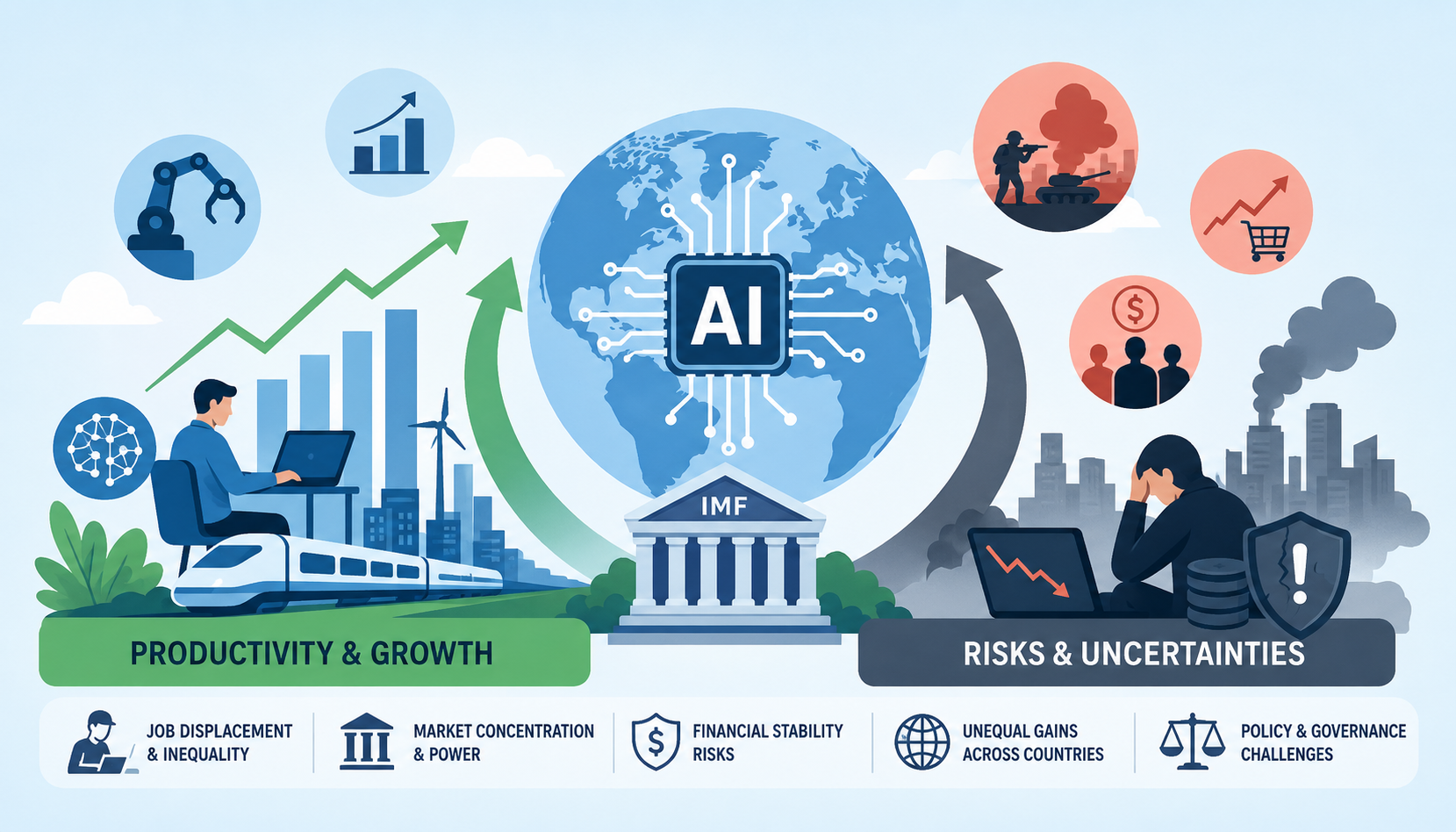

Two shocks pulling in opposite directions

The Fund frames the current moment around two forces acting with, in its words, asymmetric effects across countries. The first is a negative supply shock from the war. The second is a positive technology shock centred on AI.

On the war side, the numbers are stark but — so far — less severe than feared. After Iran shut the Strait of Hormuz on 28 February, energy prices spiked. The IMF now puts them roughly 25 percent above prewar levels, with crude oil projected to rise about 32 percent in 2026 to an assumed average of around $89 a barrel. The knock-on effect on prices is the more consequential figure: global headline inflation is expected to climb from 4.1 percent in 2025 to 4.7 percent in 2026 before easing to 3.9 percent in 2027. The Fund is blunt that the disinflation trend running since early 2024 has stalled.

What kept the damage contained was inventories. Countries drew down oil stocks to absorb the shortfall through the strait, muting the price adjustment — a buffer the IMF warns is now approaching multiyear lows.

On the technology side, the surprise ran the other way. First-quarter global growth came in at 3.0 percent annualised, above the 2.7 percent the Fund had penned in April. Most of that beat was concentrated in economies wired into the AI supply chain. The four largest net exporters of AI-related hardware — Taiwan, Korea, Thailand, and Malaysia — collectively beat expectations by an average of 4.4 percentage points, while the rest of the world came in below forecast by 0.3 point. Korea is the vivid case: it grew at 7.5 percent in the first quarter against a 1.8 percent April projection, driven by a semiconductor and AI-hardware export boom — and it did so despite heavy reliance on imported Middle Eastern energy.

That single contrast captures the Fund’s thesis. Being plugged into the AI upcycle mattered more than being exposed to the war.

A recovery that isn’t evenly shared

The steady global headline conceals a widening split beneath it. The IMF sorts countries by two axes: exposure to the war, and position in the technology value chain.

Energy exporters outside the conflict zone gain from favourable terms of trade. Economies embedded in the tech upturn hold up even when they import energy. But energy importers with little stake in the technology chain — a group that includes many low-income countries — are where activity is weakening. The Fund’s regional table makes the divergence concrete:

- Middle East and Central Asia growth collapses to 0.7 percent in 2026 before rebounding to 6.5 percent in 2027, consistent with a longer Hormuz closure and a sharper snap-back. Iraq, Kuwait, and Qatar are projected to contract in 2026, then post double-digit expansions in 2027.

- Emerging Asia’s tech exporters get upgrades: Malaysia to 4.7 percent, Vietnam to 7.5 percent, both on stronger-than-expected technology exports and data-centre activity.

- India remains among the fastest-growing majors at 6.4 percent.

- Advanced economies slow to 1.7 percent overall, with the US at 2.3 percent (barely touched by the war given its net-exporter status), the euro area at just 0.9 percent, and Japan at 0.6 percent.

The pattern is the point. AI is a narrowly shared boom sitting on top of a broadly shared shock.

Where the risks are building

The Fund’s risk assessment is more balanced than in April, but still tilted down — and the technology story is now genuinely two-sided.

Labour and inequality. The IMF’s earlier work still anchors the concern here. Its 2024 analysis, summarised in Kristalina Georgieva’s blog, found that roughly 40 percent of jobs globally are exposed to AI, rising to about 60 percent in advanced economies and falling to 26 percent in low-income countries. Around half of exposed jobs in rich economies could see productivity gains; the other half face lower labour demand, softer wages, or elimination. The Fund’s judgement was that AI is likely to worsen overall inequality — a trend Georgieva called on policymakers to address before it stokes social tensions.

Market concentration. The July update’s financial-stability box notes that equity-market concentration in AI stocks has continued to intensify, with markets carrying large AI exposures — Japan, Korea, Taiwan, and the United States — outperforming the rest. More than 80 percent of S&P 500 firms beat first-quarter earnings estimates, holding the index’s price-to-earnings ratio at a historically high level. The Fund’s warning is direct: continued strong AI capital spending could keep offsetting geopolitical headwinds, but AI hype and exuberant markets could also “sow the seeds of macrofinancial instability.”

Financial plumbing. The Bank for International Settlements has pushed this further, flagging circular financing among AI hyperscalers and the growing role of non-bank institutions — now the largest holders of advanced-economy sovereign debt, up from 44 percent in 2021 to 53 percent in 2025. BIS officials have also warned that when many institutions run similar AI models and decision rules, they may react to shocks in the same way, raising correlations and letting stress spread faster.

The scenario the IMF sketches is not that AI fails, but that expectations get repriced: if projected AI profitability disappoints, technology-heavy investment could retrench abruptly and frothy valuations could correct sharply, transmitting across borders through trade links and portfolio exposures.

The policy tightrope

The Fund’s advice reflects the double-sided setup. Central banks should hold the line on price stability — which, with inflation re-accelerating, may mean keeping real rates steady even if that requires higher nominal rates. Independence and clear communication are treated as tools in their own right. On fiscal policy, the message is to unwind energy subsidies as the shock fades and rebuild buffers rather than reach for broad-based support.

On AI itself, the IMF’s line is that the gains are real but conditional. Capturing them requires investment in skills, energy, and digital infrastructure, plus credible governance for data and cybersecurity. For low-income countries, that also means closing basic gaps in electricity and connectivity before AI productivity is even on the table.

Analyst’s View

From a country-risk and IFRS 9 vantage point, the July update is less a growth story than a dispersion story — and dispersion is where provisioning judgement lives.

Sovereign risk is bifurcating along a technology axis, not just an energy axis. The old mental model — energy exporters strong, importers weak — no longer sorts the portfolio cleanly. Korea imports Middle Eastern energy and still printed 7.5 percent. The more discriminating variable is position in the AI value chain. For a Middle East / ASEAN / Africa book, that argues for splitting the sovereign watchlist into three buckets: tech-integrated importers (Malaysia, Vietnam, Korea) where the terms-of-trade drag is being overridden; energy exporters cushioned by prices but exposed to a Hormuz re-escalation (the GCC names, where the IMF’s 0.7 percent-then-6.5 percent MENA path signals a real but recoverable stress); and energy-importing, tech-absent low-income sovereigns, where higher food and fuel prices, thinner reserves, and falling official development assistance stack up. That third bucket is where I would be testing for Stage 1-to-Stage 2 migration triggers on forward-looking indicators rather than waiting for realised deterioration.

On credit risk, the concentration cuts both ways. AI leaders are lifting index-level earnings and keeping spreads tight, which flatters aggregate credit quality and can mask weakness in laggard sectors and in the SaaS/private-credit chain the BIS is watching. The qualitative-overlay question is whether low ECL readings reflect genuine resilience or a valuation regime not yet tested by an AI-expectations repricing — a distinction worth documenting rather than letting a benign macro print flow straight through the model.

On positioning, separate the productivity thesis from the valuation. The IMF’s own framing — AI capex is boosting demand today while the productivity payoff remains ahead — is the whole risk in one sentence. Exposure premised on near-term earnings delivery in crowded AI trades carries repricing risk that the correlation dynamics BIS describes could amplify. For a long-horizon, capital-stewardship mandate, the defensible stance is patience: treat the offset as real but reversible, and size for the scenario where the two forces stop cancelling out.

The Fund’s baseline assumes Hormuz reopens from mid-July and normalises by March 2027. That assumption is doing a great deal of work. If it slips, the AI offset does not save the importers — it just widens the gap.