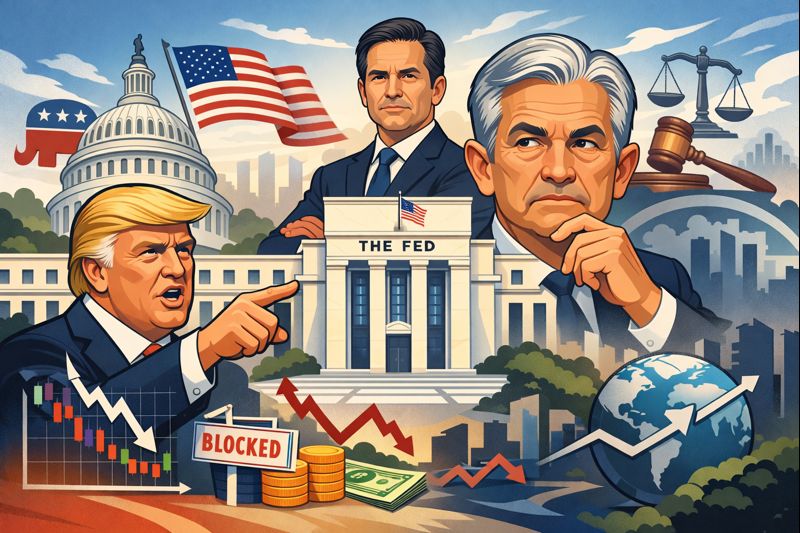

President Donald Trump’s long-running feud with Federal Reserve Chair Jerome Powell has entered a new phase — one that risks entangling the U.S. central bank in partisan conflict just as global markets are searching for policy stability. At the center of the storm is Kevin Warsh, Trump’s nominated successor, whose path to the Fed’s top job may depend less on economics than on how Washington resolves an unprecedented institutional standoff.

A Feud That Escalated to Criminal Investigation

The tensions between Trump and Powell are not new, but their intensity has reached extraordinary levels. Since Powell’s appointment in 2018, Trump has persistently criticized the Fed chair for not cutting interest rates aggressively enough, arguing that tighter monetary policy was constraining economic growth. What began as public complaints has evolved into something far more serious.

In early 2026, the Department of Justice launched a criminal investigation into Powell, ostensibly focused on cost overruns related to the Fed’s Washington headquarters renovation project. The construction budget has ballooned to $2.5 billion, well beyond initial estimates. However, Powell and many observers view the probe as a thinly veiled attempt to pressure the central bank into adopting Trump’s preferred monetary policy stance.

Powell responded with uncharacteristic bluntness, calling the investigation a “pretext” designed to force the Fed into following White House orders. This direct confrontation between a sitting president and the nation’s central bank chief is virtually unprecedented in modern American history, raising fundamental questions about the institutional boundaries between political leadership and monetary policy independence.

Enter Kevin Warsh: Background and Credentials

On January 30, 2026, Trump announced his nomination of Kevin Warsh to succeed Powell when his term as chair expires in May. At 55, Warsh brings substantial credentials to the role. He previously served as a Federal Reserve governor from 2006 to 2011, giving him front-row experience during the 2008 global financial crisis. During that turbulent period, Warsh was instrumental in coordinating emergency liquidity facilities and crisis-response measures.

After leaving the Fed, Warsh worked at Morgan Stanley and has since been affiliated with Stanford’s Hoover Institution and Graduate School of Business. His background combines Wall Street experience with academic engagement, and he represented the Fed at G-20 meetings during his previous tenure, giving him international policy experience.

Warsh was previously a finalist for the Fed chair position in 2017 when Trump ultimately selected Powell. Trump has since stated he made a mistake not choosing Warsh then — a comment that takes on new significance given the subsequent deterioration in the Trump-Powell relationship.

The Philosophy Question: What Does Warsh Believe?

Historically, Warsh established a reputation as a monetary policy “hawk” — someone who prioritizes fighting inflation over maximizing employment and growth. During his earlier Fed tenure, he publicly opposed the second round of quantitative easing in 2011, expressing concern about balance sheet expansion and long-term inflation risks. He resigned shortly after that policy disagreement.

Warsh has also been a vocal critic of what he views as the Fed’s mission creep into areas like climate policy, arguing these issues fall outside the central bank’s core mandate. He has called for “regime change” at the Fed and advocated for shrinking the institution’s $6.6 trillion balance sheet.

However, a notable shift has occurred in recent years. Since emerging as a potential Powell successor, Warsh has aligned himself more closely with Trump’s position, publicly arguing for lower interest rates. This evolution in his stance has created uncertainty about which version of Warsh would actually govern once in the chair: the hawkish inflation fighter of 2006-2011, or the more dovish voice of 2025-2026.

The answer matters enormously for markets and the global economy. A truly independent Warsh focused on price stability could disappoint Trump’s expectations for aggressive rate cuts. But a Warsh willing to subordinate monetary policy to White House preferences would represent a fundamental transformation of Fed governance.

The Senate Confirmation Bottleneck

Warsh’s path to confirmation is complicated by the very controversy surrounding his nomination. Senator Thom Tillis, a Republican member of the Senate Banking Committee, announced he would oppose Warsh’s confirmation until the DOJ investigation into Powell is “fully and transparently resolved.” Tillis declared that “protecting the independence of the Federal Reserve from political interference or legal intimidation is non-negotiable.”

This creates a significant obstacle. Without Tillis’s support, Warsh’s nomination may struggle to advance through the Banking Committee, where Republicans hold a narrow majority. The refusal of even a single Republican on the panel could prevent a favorable committee recommendation to the full Senate.

Trump responded by insisting the investigation should continue, telling reporters on February 2 that U.S. Attorney Jeanine Pirro should “take it to the end and see.” This stance appears to harden the political standoff rather than provide the “off-ramp” some analysts believe Trump needs to facilitate Warsh’s confirmation.

Democratic Senator Elizabeth Warren has also signaled strong opposition, arguing that “no Republican purporting to care about Fed independence should agree to move forward with this nomination.” She characterized Warsh as someone who “cared more about helping Wall Street after the 2008 crash than millions of unemployed Americans” and suggested he has “passed the loyalty test” to Trump.

The confirmation process thus becomes a test not just of Warsh’s qualifications, but of Congress’s willingness to defend institutional norms around central bank independence.

Why Fed Independence Matters

The principle of central bank independence rests on a straightforward logic: monetary policy often requires difficult, politically unpopular decisions. Fighting inflation may require raising interest rates to deliberately slow economic growth — not the kind of policy an elected official wants to champion before an election.

When central banks operate under political pressure, the temptation to prioritize short-term economic stimulus over long-term price stability becomes overwhelming. This dynamic has repeatedly led to elevated inflation in countries where central banks lack genuine autonomy.

The United States has maintained relatively strong Fed independence since the 1951 Treasury-Fed Accord, which established the central bank’s freedom from direct political control. This institutional arrangement is widely credited with helping the U.S. achieve price stability and credible monetary policy for decades.

A Fed chair who is seen as a presidential loyalist, appointed specifically to deliver the policy outcomes the White House desires, would fundamentally alter this framework. Markets would question whether Fed decisions reflected genuine economic analysis or political calculation. This uncertainty itself would be destabilizing, potentially increasing inflation expectations and raising long-term borrowing costs.

Moreover, the international dimension matters considerably. The Federal Reserve’s decisions ripple through global markets because of the dollar’s role as the world’s reserve currency. Foreign investors, central banks, and governments all make decisions based on assumptions about U.S. monetary policy credibility. A politically compromised Fed would undermine confidence in dollar-denominated assets and potentially accelerate the search for alternative reserve currencies.

Market Reactions: A Mixed Verdict

Financial markets delivered a nuanced verdict on Warsh’s nomination, with reactions varying across asset classes. The most dramatic moves occurred in precious metals markets. Gold prices plunged by approximately 9%, while silver dropped an extraordinary 28% following the announcement. These metals had been rallying for months as investors hedged against fears of Fed independence erosion and dollar debasement. Warsh’s nomination, paradoxically, triggered a reversal of this “debasement trade” because investors viewed him as more credible and institutionally minded than alternative candidates.

The U.S. dollar rallied following the announcement, gaining 0.8% against a basket of currencies. This response suggested market confidence that Warsh would not simply capitulate to demands for unlimited monetary easing. Currency traders appeared to price in the expectation of a Fed chair who would maintain some degree of policy discipline.

Equity markets showed more modest negative reactions. The S&P 500 declined 0.4% on the day of the announcement, while the Nasdaq fell 0.9%. These relatively contained moves indicated that investors were not panicking, but were recalibrating expectations for future monetary policy.

Treasury yields showed a “steepening” pattern, with short-term yields declining while long-term yields rose. This curve movement suggested traders expect near-term rate cuts (consistent with Trump’s demands) but harbor concerns about inflation control and fiscal sustainability over longer horizons.

Analysts at major institutions offered cautiously optimistic assessments. David Bahnsen of The Bahnsen Group noted that Warsh “has the respect and credibility of the financial markets.” Others emphasized that Warsh’s experience and hawkish track record provided some reassurance about his potential independence, even while acknowledging he would face enormous pressure from the White House.

The market response essentially reflected a bet that Warsh represents a middle path: someone with close ties to Trump who might accommodate some near-term easing, but who also possesses sufficient institutional credibility and policy experience to resist the most extreme political pressure.

Global Spillovers and International Implications

For international observers, the Trump-Powell confrontation and Warsh nomination carry significant implications. The Federal Reserve’s policy stance influences capital flows worldwide. When the Fed signals it may become more dovish, emerging market currencies often strengthen as investors search for higher yields in riskier assets. Conversely, expectations of tighter U.S. monetary policy or dollar strength can trigger capital flight from developing economies.

The uncertainty surrounding Fed independence creates an additional risk premium. If global investors cannot reliably predict Fed decision-making because of political interference, they will demand higher returns to compensate for this unpredictability. This manifests as wider credit spreads for both U.S. and international borrowers.

European and Asian central banks are watching developments closely. The European Central Bank, Bank of Japan, and other major central banks coordinate with the Fed on various issues, including currency swap lines that serve as crisis backstops. A politicized Fed would complicate these relationships and could reduce international cooperation during future financial stress.

China and other nations seeking to reduce dependence on dollar-based financial infrastructure may view the current turmoil as validating their concerns about dollar system stability. The Belt and Road Initiative, yuan internationalization efforts, and digital currency development all gain additional justification if the Fed appears compromised by political pressure.

What Happens Next?

The timeline for resolution is compressed. Powell’s term as chair ends on May 15, 2026, giving the Senate just over three months to hold hearings, vote in committee, and confirm Warsh — assuming the DOJ investigation is resolved or Tillis’s objection is overcome.

Several scenarios are possible. Trump could end the Powell investigation as a concession to facilitate Warsh’s confirmation, though his recent statements suggest resistance to this path. Alternatively, Senate leadership might attempt to force a floor vote without committee approval, though this would be procedurally difficult and politically divisive.

Powell could potentially step down before his term expires if Warsh is confirmed, or he might choose to remain in place through May 15 to emphasize the principle of serving out appointed terms regardless of political pressure. Speculation suggests Powell is considering staying to the end as a statement about institutional independence.

Meanwhile, the Federal Open Market Committee continues making policy decisions with Powell at the helm. At its most recent meeting in early 2026, the FOMC held interest rates steady. This decision reflects the committee’s data-dependent approach and suggests that despite political pressure, the broader membership remains focused on inflation control.

The Broader Stakes

The Warsh nomination represents more than a personnel change. It crystallizes fundamental questions about the relationship between democratic governance and technocratic expertise. Should elected officials have greater influence over monetary policy on the grounds of democratic accountability? Or does effective central banking require insulation from political pressure precisely because optimal policy often conflicts with short-term political incentives?

There are no simple answers to these questions. Throughout American history, periodic tensions between presidents and the Fed have been inevitable given the central bank’s enormous influence over economic conditions. But the current confrontation has crossed new lines — criminal investigations, public demands for rate cuts, threats to reshape the institution’s governance.

For investors, policymakers, and citizens worldwide, the coming months will reveal whether American institutions can withstand this pressure while preserving the credibility that underpins the dollar’s global role. Kevin Warsh inherits not just the Fed chairmanship, but also the weight of defending — or redefining — what central bank independence means in an era of intensifying political polarization.

The resolution of this standoff will echo far beyond Federal Reserve Board meetings. It will shape inflation expectations, currency valuations, and international confidence in the U.S. economic system for years to come. Markets are watching, Congress is divided, and the world is waiting to see whether the institution that has anchored global finance since World War II can navigate its most fraught leadership transition in modern history.