Japan appears to be preparing to tighten how it manages the financial resources behind yen intervention, a move that could sharpen market attention on Tokyo’s ability to defend the currency during periods of renewed yen weakness.

Why Japan’s Yen Intervention Toolkit Is Back in Focus

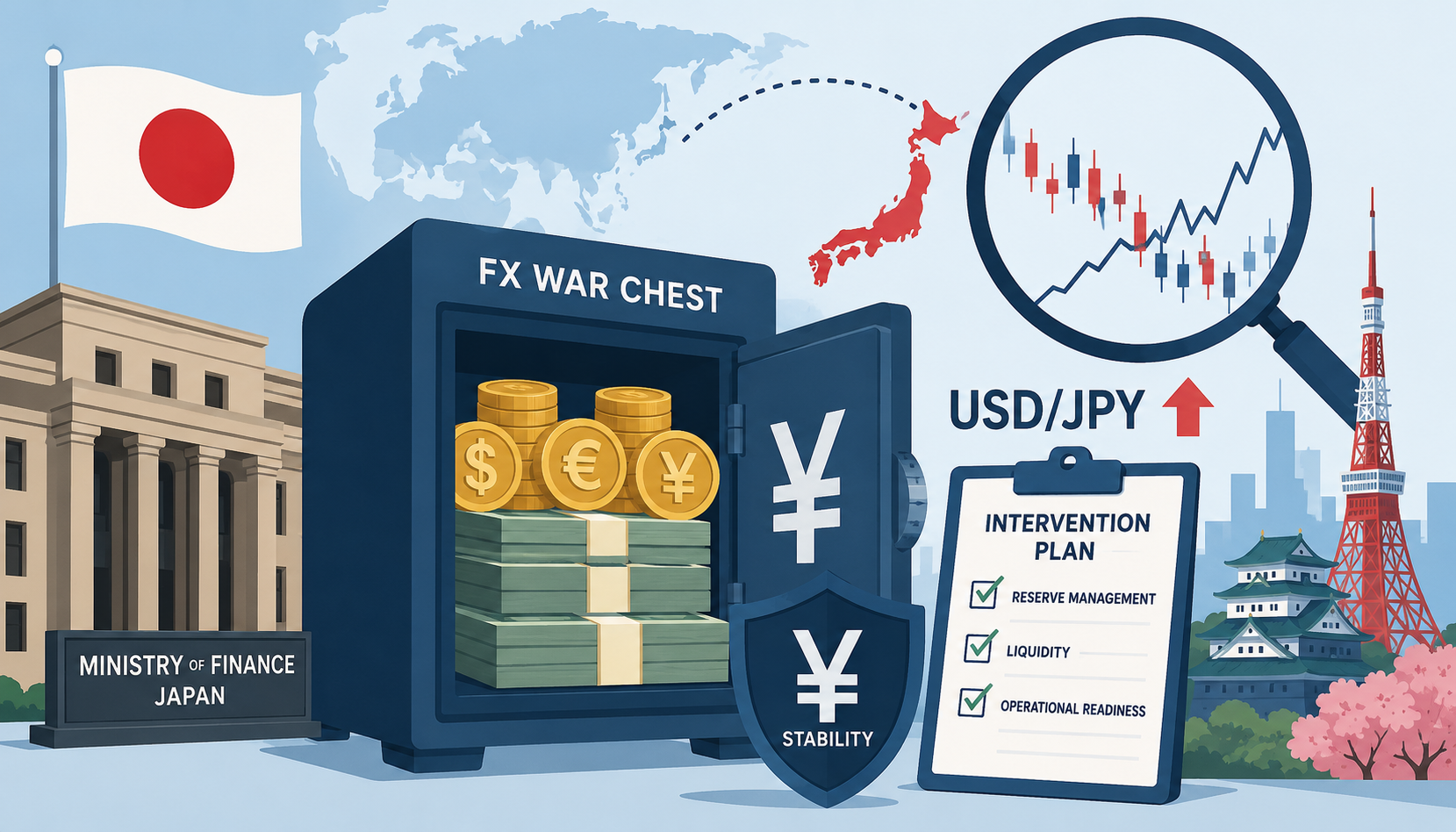

On June 24, Reuters reported that the government plans to study ways to improve management of its foreign exchange reserves — the roughly $1.3 trillion pool that doubles as a war chest for yen intervention — citing a draft growth strategy it had reviewed. The draft language is cautious: the government would examine the merits of improving management and making more effective use of public-sector assets, including the foreign exchange fund special account, taking into account their intended purposes. No specific reallocation is spelled out.

The timing is what makes it interesting. The draft is a centerpiece of Prime Minister Sanae Takaichi’s agenda and her “responsible proactive fiscal policy” line, and it lands only weeks after Tokyo spent more on currency support than in any single month on record. Intervention is not just a political signal. It depends on available foreign-currency assets, on timing, on coordination with partners, and on market credibility. A plan to manage the war chest more actively touches all of those.

What “FX War Chest” Means

The phrase usually refers to the foreign-currency reserves authorities can draw on when they sell foreign assets and buy yen. In Japan’s case the bulk of those reserves sit in the foreign exchange fund special account (外国為替資金特別会計, or gaitame tokkai), which the Ministry of Finance describes as the vehicle that holds foreign assets acquired through past intervention, financed by issuing short-term government bills.

Two features matter for what follows. First, the account’s stated investment principle is to put safety and liquidity first, and to pursue returns only within that constraint — a deliberate ordering, because the assets exist to be deployed at short notice. Second, the division of labor is specific: the Ministry of Finance decides intervention policy, while the Bank of Japan executes operations as its agent. When you read that “Japan intervened,” it is the MOF’s call, run through the BOJ’s trading desk.

The reserves themselves are large and concentrated. They are believed to be invested mostly in U.S. Treasuries, accumulated over years of dollar-buying intervention, and since 2022 Tokyo has funded yen-buying operations partly by selling some of those Treasuries.

Why Better Management Matters

Reserve management is relevant even before a single yen of intervention is spent. Markets care not only about whether Japan acts, but about whether the authorities have enough flexibility, liquidity, and political backing to act decisively.

There is also a domestic budget angle that the draft makes explicit. The surplus generated by the reserves — including interest income on U.S. Treasuries — is transferred to the general account and used to fund the state budget. Takaichi has publicly described the reserves as a beneficiary of the weak yen that was “performing very well,” a remark some officials read as a signal she hoped to tap the surplus to help fund a plan to suspend the consumption tax on food. Separately, some lawmakers from both ruling and opposition camps have floated folding the reserves, the central bank’s ETF holdings, and pension assets into a sovereign wealth fund chasing higher returns.

That is where the tension sits. Squeezing more yield out of the reserves and keeping them instantly available for a currency defense are not the same objective. Government officials quoted in the report pushed back on the more radical ideas, calling a drastic change to the portfolio unrealistic precisely because the reserves are held as a ready source of funds for intervention.

The Market Context: Yen Weakness and Policy Divergence

The backdrop is a yen near multi-decade lows. Through June 2026 the currency has traded in the ¥160–161 area against the dollar (the Bank of Japan publishes daily reference rates), levels not seen since the late 1980s. The proximate drivers are familiar: a wide interest-rate gap with the United States and a Federal Reserve in no hurry to cut, set against a Bank of Japan that is normalizing only gradually.

The BOJ did move. It raised its policy rate to 1.00% at its mid-June meeting, its first hike since December 2025, partly to lean against yen weakness. But even at 1%, the differential with U.S. rates remains large, and that gap is the gravitational pull behind the yen’s slide. Layered on top is the energy shock from the 2026 Middle East conflict, which pushed oil sharply higher before a ceasefire in mid-June and added to Japan’s import bill — another weight on the currency.

It was in this environment that Tokyo stepped back into the market. According to Ministry of Finance data, intervention from April 28 to May 27 totaled ¥11.73 trillion (about $73.6 billion) — the largest monthly yen-buying operation on record, surpassing the roughly ¥9.79 trillion spent over a comparable stretch in 2024, and the first intervention since that year. The trigger was the yen sliding past ¥160.72 to the dollar. The cost showed up immediately in the reserves: MOF figures for end-May put holdings at $1,305,874 million, down about $77 billion from April — a 5.58% drop, the steepest since the data series began in 2000.

Policy Credibility and Signaling

A draft plan can function as a signal to traders even without any new operation behind it. If Tokyo is seen to be sharpening the readiness of its war chest, the perceived cost of betting one-way against the yen rises. That, in turn, can make speculative short positions a little more expensive to hold.

But the signal cuts both ways. The record May intervention drew commentary that the yen kept sliding anyway, which fed the long-running argument that unilateral intervention has limits. Improving the management of the fund does nothing to close the rate gap. It can buy time and smooth disorderly moves; it does not change the carry math that makes the yen a funding currency. Markets know this, which is why operational readiness tends to affect the speed of a move more than its direction.

Risks and Constraints

A few constraints are worth keeping in view, and I’d separate the well-established ones from the more speculative.

- Fundamentals can overwhelm intervention. As long as the rate differential and energy-driven inflation weigh on the yen, reserve management may slow the trend without reversing it. The sheer scale of the market is part of the reason — the BIS estimated global FX turnover at roughly $9 trillion a day in its 2025 survey, against which even a $74 billion operation is small.

- International scrutiny. Japan sits on the U.S. Treasury’s currency monitoring list, and the two governments’ finance ministers reaffirmed that intervention should be reserved for countering excess volatility and disorderly moves, with monthly disclosure. Funding yen-buying by selling U.S. Treasuries also nudges U.S. yields higher, a side effect Washington watches closely.

- The surprise factor fades. Repeated, telegraphed intervention loses some of its shock value, and a fund managed more for yield could — speculatively — end up marginally less liquid at the moment it is needed most.

What Investors Should Watch Next

Concrete indicators worth tracking from here: the MOF’s monthly and quarterly intervention disclosures, which in early August will give a day-by-day breakdown of the spring operations; month-end reserve figures for signs of further drawdown; USD/JPY volatility around the ¥160 line; the next U.S. Treasury foreign exchange report and any commentary from Secretary Bessent; the BOJ’s rate path into the autumn; and the final text of the growth strategy, to see how far the “better management” language actually goes.

Analyst’s View

From a country-risk and risk-management seat, the headline number — a $77 billion reserve drawdown in a single month — looks dramatic but is not, on its own, a solvency story. Japan still holds roughly $1.3 trillion in reserves and remains the world’s largest net external creditor, so reserve adequacy is not the binding constraint here. The binding constraints are credibility and the rate gap, neither of which a fund reallocation fixes.

The more interesting risk is the internal contradiction in the draft itself. “Boost returns” and “keep the war chest instantly deployable” pull in opposite directions, because reaching for yield typically means trading away the safety and liquidity that a currency defense relies on. For anyone modeling sovereign or contingent liquidity, the variable to watch is governance: how any reallocation is structured, and whether the liquidity profile of the account is preserved. A sovereign-wealth-fund framing would be the clearest red flag on that axis.

On positioning, the practical takeaway is narrow. Improved operational readiness raises the carrying cost of one-way yen shorts and can punish complacency around ¥160, but it does not alter the underlying carry that has driven the trade. Intervention smooths; it does not reverse. And the external coordination layer — the U.S. monitoring list, the joint commitment to intervene only against disorderly moves, and the feedback loop from Treasury sales into U.S. yields — effectively caps how aggressively Tokyo can lean. The war chest is being polished, not enlarged, and the market is likely to price it accordingly.