U.S. inflation is no longer behaving like a problem the Federal Reserve can comfortably wait out. The latest data show price pressure back at a three-year high while consumers keep spending — a combination that quietly kills the case for rate cuts and puts the next hike, not the next cut, on the table.

That is not a forecast. It is what Fed officials themselves signalled a week before the spending data landed. And it changes the global backdrop for bonds, the dollar, and anyone funding in dollars.

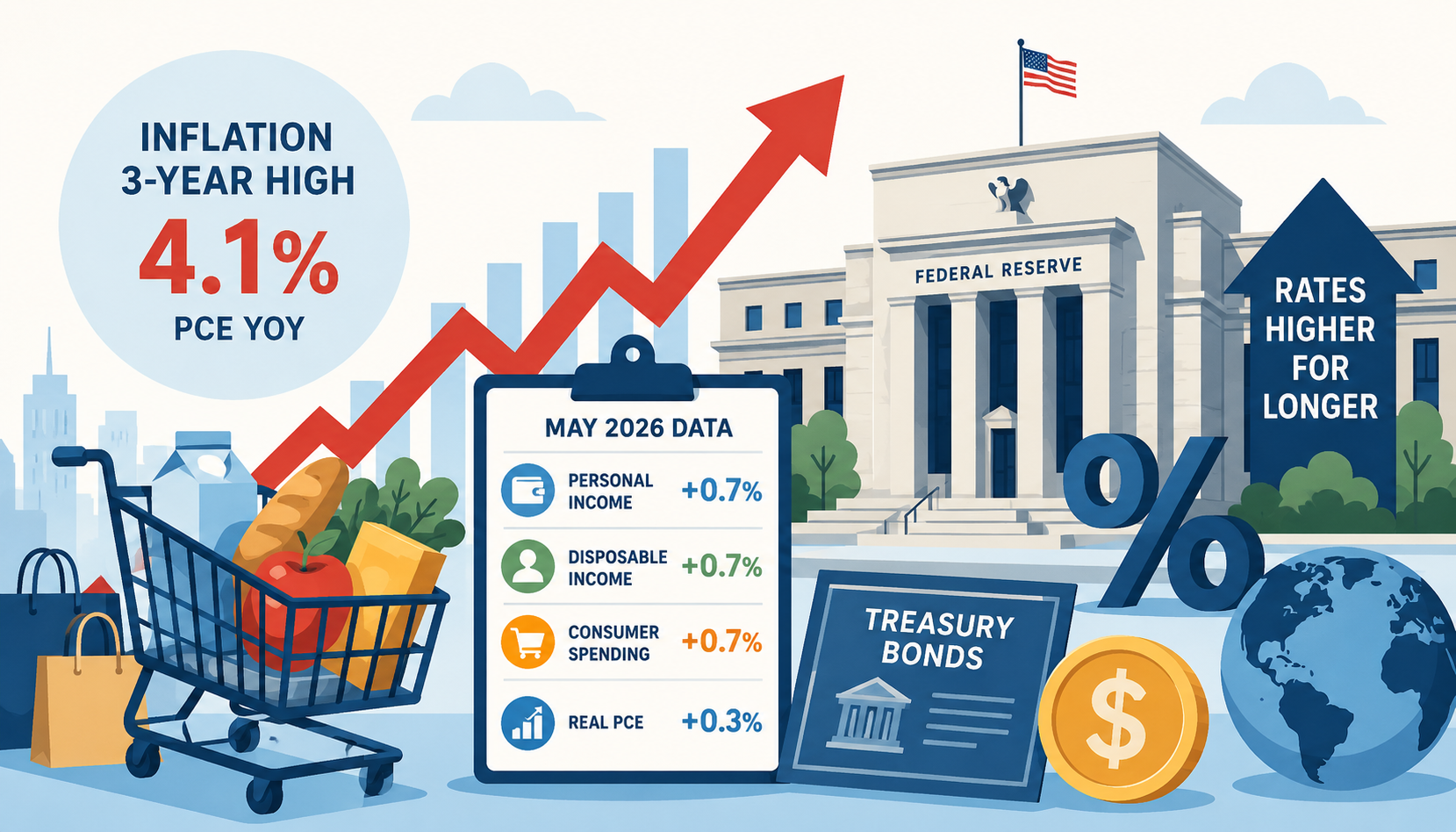

The Data: Hot Prices, and Spending That Won’t Quit

Start with the release that closed the picture. On June 25, the Bureau of Economic Analysis reported that in May personal income rose 0.7%, disposable income rose 0.7%, and personal consumption expenditures (PCE) rose 0.7%. Crucially, real PCE — spending adjusted for inflation — rose 0.3%. Households were not just paying more for the same basket; they were buying more.

The price side was just as firm. The PCE price index, the Fed’s preferred inflation gauge, rose 0.4% on the month and 4.1% over the year. Core PCE, which strips out food and energy, rose 0.3% on the month and 3.4% year-on-year. The personal saving rate slipped to 3.0%, the kind of number that says households are leaning on income, not pulling back.

A few days earlier, the Bureau of Labor Statistics had set the headline. The Consumer Price Index rose 4.2% over the 12 months ending in May — the highest annual reading since April 2023, hence the “three-year high.” So you have two independent inflation measures, CPI and PCE, both well north of target, and spending that refused to roll over. That is the uncomfortable shape of this data.

Why 4% Inflation Is a Problem the Fed Can’t Wait Out

The Fed targets 2% inflation, measured by PCE. A 4.1% headline reading is more than double that. Inflation has now run above the 2% goal for five straight years, and the public’s patience — and the central bank’s credibility — is not infinite.

The deeper worry is not the level on any single month. It is persistence. When inflation is driven by a one-off shock, policymakers can look through it and wait for the math to roll off. When spending is still growing in real terms and the labor market is intact, looking through becomes a gamble: the shock can seep into wages, services, and expectations, and stay.

Oil Shock or Demand Problem? Both — and That’s the Trap

Here is where it gets analytically interesting, and where a lazy reading goes wrong.

The May inflation spike is, mechanically, an energy story. The BLS reported that energy prices rose 23.5% over the year and gasoline jumped 40.5%, with the energy index alone accounting for more than 60% of the monthly increase in the all-items CPI. The driver is the disruption to Middle East oil supply tied to the Iran conflict. On its face, that is exactly the kind of supply shock central bankers are trained to ignore.

But two facts complicate the “just oil” narrative. First, core CPI was only 2.9% year-on-year — contained, not spiraling — which tells you the underlying trend is calmer than the headline. Second, and pulling the other way, real spending grew and the labor market stayed firm: nonfarm payrolls added 172,000 jobs in May and unemployment held at 4.3%.

So the question is not “supply or demand.” It is whether an energy shock landing on top of resilient demand is safe to look through, or whether it hardens into something stickier. That is a genuinely hard call, and reasonable people on the committee disagree.

The Fed Already Blinked Hawkish

This is the part the headlines about May inflation tend to bury: the Fed has already moved.

The June 16–17 FOMC meeting was the first chaired by Kevin Warsh, sworn in on May 22 after Jerome Powell’s term as chair ended (Powell stays on as a governor and voting member). The committee held the funds rate at 3.50%–3.75% by a unanimous 12–0 vote — but the tone changed sharply.

The statement was gutted to roughly 130 words, stripped of forward guidance, and ended on a line the old Fed would never have written so flatly: “The Committee will deliver price stability.” The easing bias was gone.

The projections went further. In the June Summary of Economic Projections, the median dot for the end of 2026 moved up to 3.8%, from 3.4% in March — a flip from a committee that three months earlier still penciled in a cut, to one whose median now implies a hike. Officials raised their 2026 headline PCE projection to 3.6% and core to 3.3% (both 2.7% in March), trimmed GDP to 2.2%, and nudged unemployment down to 4.3%. Of 18 participants, 17 judged inflation risks to be tilted to the upside.

There is a nuance worth flagging. Warsh has personally argued that supply-shock inflation should generally be looked through, and he declined to submit his own dot. Yet the committee he now chairs pivoted hawkish anyway — a sign the hawkishness is being driven by the resilience of demand and the breadth of upside risk, not just the oil price. As Goldman Sachs Asset Management’s Kay Haigh put it after the meeting, the shift was not only about energy.

What It Means for Markets

The mechanics flow from one idea: the “soft landing plus rate cuts” trade is being repriced toward “higher for longer, with hike risk.”

- Treasury yields. Higher-for-longer expectations, plus the dot-plot flip, pressure front-end yields in particular. Short rates jumped and equities fell on the day officials penciled in a 2026 hike.

- The dollar. A more hawkish Fed, especially relative to easing central banks elsewhere, is a tailwind for the dollar — though positioning and risk sentiment can blunt the move, so this is a lean, not a certainty.

- Equities. Higher discount rates weigh on long-duration growth names, while firm real spending supports near-term earnings. The net depends on which force the market chooses to price on a given week.

- Emerging markets. This is the channel that matters most beyond U.S. borders. A firmer dollar and higher U.S. yields tighten external financing conditions, widen sovereign spreads, and raise the cost of rolling dollar debt.

Global Spillovers

A hawkish Fed exports tighter financial conditions. It lifts the cost of dollar funding worldwide, raises the local-currency bill for commodity importers already paying up for oil, and pulls capital toward U.S. assets and away from higher-risk markets. For economies running on external financing, the U.S. inflation print is not a foreign headline — it is an input into their own cost of money.

Analyst’s View

From a country-risk and credit-risk seat, the signal in this data is about the reaction function, not the single print.

Credit risk: the refinancing window is staying expensive. If the Fed holds higher for longer — and now flirts with a hike — floating-rate and near-term-maturity borrowers lose the relief that a cutting cycle would have brought. Watch U.S. corporate spreads, leveraged-loan coupons resetting against a 3.5%+ base rate, and consumer credit quality as a 3.0% saving rate leaves households with thinner buffers. The names that planned around 2026 cuts are the ones to stress-test first.

Sovereign and country risk: dollar tightening is the live channel. Emerging markets with high dollar-denominated debt, thin reserves, or wide current-account deficits face the familiar squeeze — stronger dollar, higher refi costs, wider spreads — made worse where the oil shock is also inflating the import bill. The same energy spike that is lifting U.S. CPI is a terms-of-trade hit for oil importers and a windfall for exporters; country risk here is not uniform, and it should be scored issuer by issuer.

Positioning: disinflation trades carry asymmetric risk. Portfolios built for “inflation rolls over, Fed cuts, carry works” are now leaning into a committee that says the opposite. The exposure to reassess is duration, growth-equity multiples, and EM carry. The risk is not one hot month; it is that the market was pricing a policy path the Fed has just walked away from.

One honest caveat: much of this hinges on oil. A genuine de-escalation in the Middle East that pulls energy prices back could let core inflation peak this quarter and hand the Fed its “look-through” justification after all. That path stays open. But it is a bet on geopolitics — and building a credit or rates view on a hoped-for ceasefire is exactly the kind of single-variable dependence a risk manager is paid to flag, not to assume.